For employers, brokers, and employees

Pamela Whitfield – 6/23/2022

True confession: I have had a love affair with the accident plan for close to 30 years. Who wouldn’t love a plan that has no age bands, no health questions, ripe with benefits that pay CASH to policyholders and their families in addition to getting paid for just getting a no-cost preventative test? Throw in low cost as well as the ability to pre-tax thus resulting in even lower net premiums…aren’t you getting a little excited?

All joking aside, we all know that accidents are serious and always happen without warning. 1 in 4 people will experience an injury or illness that prevents them from earning an income in their careers. Accidents are the leading cause of death in young people and my employee websites contain more facts around accidents www.elite-vb-hawaii.com / www.elite-vb-alaska.com as the risksare real.

Given that my agency specializes in post-pandemic virtual voluntary benefit programs as well as teach HR and brokers about the impacts of Covid at the workplace, I felt it important to list the top 10 reasons why an accident plans is an easy choice for every employer to offer.

While I listed a few of the obvious benefits/reasons in the first paragraph, I will expand to more sophisticated applications for the accident plan belowas this can be a very powerful product with many applications. With my focus being “how to leverage voluntary benefits to aid in RECRUITING and RETENTION”, I can’t think of an easier choice than ensuring an accident plan gets on the list so let’s jump right in starting

- No age bands: This is a very important feature with most accident plans/carriers as many insurance products ARE age banded. Family and spouse coverage is also valuable and important, but the big advantage here is that there are no age bands. Employees up to age 80 could purchase it. It’s great that employees qualify, but it’s bigger than that. Let’s look at three advantages to this feature:

- Aging workforces are coming back: Inflation is causing some Americans to have to go back to work. People that either can’t afford to retire or must face coming back to work to pay bills will be able to purchase this plan (at the same premium as an employee aged 25). Over the years, I have seen older employees not want to attend meetings as they assumed they wouldn’t qualify for any of the benefits due to their age. This is not the case with the accident plan which means more employees qualify for the plan (which equates to higher participation) but the other reason is employees can port the plan (with zero increase in premium/benefits) and keep it if they get injured in their later years.

- Easier to fund (employer-paid): When an employer is considering funding the accident plan, knowing that EVERY employee is “x” amount per month is easier to budget for than calculating various age bands/changing age bands. Not to mention, everyone qualifies, so you’re there is no concern about excluding some employees due to age.

- Diversity, Equity & Inclusion (DEI): Talk about inclusion: when ALL employee’s quality with zero health questions, zero qualifications,no premium increase based on age or gender, then I would say that the good old, trusted Accident plan checks the DEI “box”.

- No health questions (“guarantee issue”): This feature is standard with all carriers and while many group carriers also waive health questions during a new open enrollment, we can’t discount the value of offering voluntary benefit programs that is filed without health questions to qualify. This feature checks the “DEI” box as well as the “employer-paid” box as this means no health questions applies tothe entire family (even those who may be disabled, undergoing cancer treatment, those who may be in questionable health, etc.).

- Eligibility for the benefit may be 20 hours (versus 30 hours) for part-time workers:This feature can be important for employers who have part-time workers. Accident plans that cover employees who work 20 hours or more can be an invaluable benefit to employers who have employees who work half/part-time as it might be the only benefit that they are both offered and can qualify for. Often these employees may not qualify for medical coverage (due to hours worked) meaning it can be a critical benefit for part-time works as those may be the ones who need it the most…those without medical.

- CASH benefit paid directly to employee (Emergency Room expenses is the biggest cause of medical debt): We know that this feature is typical with voluntary benefits, but it’s the reason that employees purchase it: to lessen their financial risk due to out-of-pocket costs. This might not be as important in Hawaii (where out-of-pocket costs are less than Alaska for example) but I would suggest that it’s important to understand what insurance is: risk management. We purchase insurance that makes good (financial) sense to us and our family. We have all seen someone get in a bad accident, the treatment is extensive and results in missing work and the bills pile up. Without robust disability coverage when an off-job-injury occurs, their paycheck might stop and thus a downward financial spiral (60% of bankruptcies are due to medical debt). Bottom line: medical carriers will NEVER pay cash to their policyholders makingthis plan ideal for companies that have medical (especially those with a high deductible) but especially those with NO medical coverage (keep reading and you’ll see why even someone with no out-of-pocket expense might select this plan).

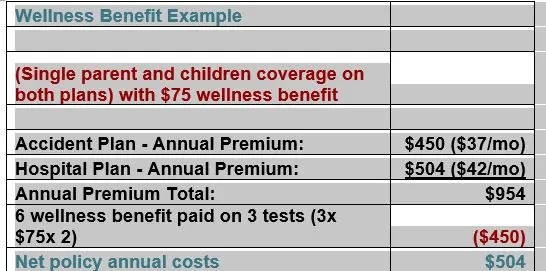

- Pays CASH benefits for preventative tests: Paying an annual health screening/wellness benefit per person is a feature on an accident plan that is standard. It can be optional (depending on the carrier) as well as the amount of the wellness benefit to be paid per person (typically from $50-100). In addition, one carrier (Assurity) will pay up to TWO benefits per yearfor up to two policyholders. Why this feature is vitally important now, in our post-pandemic era, is because Americans are still behind in their preventative tests due to pandemic lockdowns, fear of contracting the virus, difficulty in setting an appointment, and more. We know how important preventative screenings are: early detection saves lives and lowers cost for treatment.

Annual screenings are important for both the employer and the employee. Employers with self-funded plans want to encourage annual screenings as a long-drawn-out breast or colon cancer treatment due to advance stage of diagnosis can impact the company’s bottom line. But another reason is also important: employees not only LOVE getting paid on a policy without being injured, but the payments can dramatically LOWER the true cost of the policy.

Let’s look at this scenario which I lay out in my Continuing Education classes on the impact of a $75 wellness benefit paid with two policies and three policyholders (employee and two children):

This is powerful. Talk about a “win-win”: the employee is incentivized to get their preventative tests, the benefit comes to the employees to spend as they see fit and, depending on the benefit amount, it can LOWER the overall cost of the policy by 50%.

- Ability to pre-tax the premium: a “win” for the EMPLOYER and EMPLOYEE: Accident and hospital plans are two voluntary benefits that are “safe” to pre-tax without triggering a taxable event upon the payout. We know that pre-taxing any premiums benefits the employee as the premium is taken out BEFORE all taxes. If you are in a 25% tax bracket, the “net” premium on each paycheck is lowered by 25%. This is substantial. The employee can use the savings to buy more coverage, but the other “winner” is the employer. They also save on matching FICA premiums. Thus, the more pre-tax premiums, the lower the company’s bottom line and the true net deduction is lowered by a quarter.

- Carriers providing Post-Pandemic benefits that matter:Many employers have an accident place and rarely “upgrade” the plans. This is a shame because there are carriers / plans on the market now that offer rich benefits that were specifically added due to Covid. The workplace is different, employees have new needs and below is a sample of accident benefits that are standard with one carrier with lower rates than traditional carries (Aflac, Colonial, etc.):

- Telemedicine

- PTSD

- Gunshot wound

- Increased benefit for children injured in organized sports events

- Childcare benefit when hospitalized

- Accidental Death benefits include benefit for secondary education

- Accidental Death benefit increase when using a seatbelt

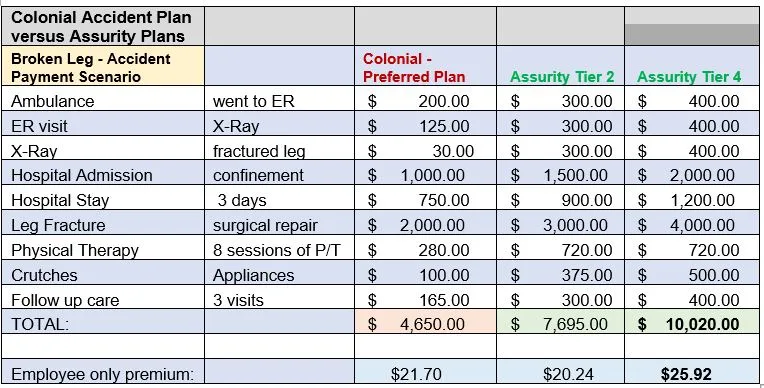

- Higher Payouts / Lower Premiums: This is an obvious reason to replace an older accident plan with carriers that have robust benefits and lower premiums. Below shows the premium and payouts for Colonial’s Preferred Individual Plancompared to Assurity’s Tier 2 and Tier 4 plans (they offer “dual option” plans that is also a reason to switch out an old plan as two options are better than one in some cases). You can see the payout for Assurity Plan would be 100+% higher with a mere $4 more per month (or 16% increase) of premium:

It’s simple: if there is a carrier in place for 5+ years and there hasn’t been an evaluation of other carriers on the market to bring in NEW features and LOWER premiums, it’s time. Inflation is starting to wreak havoc on families already. By upgrading their voluntary accident plans, you’re putting greater money in their pockets with zero cost to them, and if you lower the premium for the same plan, you’re giving them a raise. Either way, improving the benefits on an accident plan is a no-brainer while also helping with retention and recruitment.

- Accident Plans can lower Workers Compensation claims(either with employee or employer-paid): Of employers who offer supplemental insurance, over half offer Accident Insurance. More and more employers are seeing the value in PAYING for an off-job only accident benefit, so let’s look at the data supporting this:

- In a 2016 Aflac survey of 1500 employers, those who offered an accident plan to their employees that paid cash benefits, 51% saw a decrease in workers’ comp claims

- 40% saw a significant reductionwith

- 34% seeing a VERY significant reduction of workers comp claims (a reduction of 75% or more)

- Average workers’ comp claim reduction with large employers offering a voluntary accident plan AND short-term disability showed a reduction of 55%

In summary, voluntary benefit strategies designed to risk management are linked to better outcomes on workers’ comp abuses while directly positively impacting a company’s bottom line.

- Gunshot Wound Benefit: There were over 45,000 deaths due to guns last year, more than 700 children died of gunshot in America between January and May) and with over 400 million guns in America, I would say ensuring we due to the risks and impact of a gunshot wound is a priority. While it isn’t a comfortable topic, I believe it is time to revisit the power of an accident plan that includes a gunshot wound benefit. I recall employees giggling when we brought it up, but this overlooked benefit is nothing to laugh at. Assurity is one of the carriers that pays a $2k gunshot wound on its Tier 4 Accident plan (that costs less than a dollar a day). I ran some numbers on a typical hospital stay due to an abdominal gunshot wound where the person spends 10 days I the hospital and it’s close to $20,000. This is paid directly to the victim (or their covered family members). If the policyholder died due to gunshot, their beneficiary would receive over $80k plus $2k. Please revisit this important employee-benefit for your staff as it’s never just the out-of-pocket costs that these plans cover. When someone is in the hospital, their paycheck stops. If your child is in the hospital, you aren’t working. This benefit is so powerful that I would recommend employers PAY for this benefit. Talk about inclusion: because there are no age bands or health questions, it’s easy to fund and it would provide tremendous PEACE OF MIND. My heart is heavy with these statistics that are our new post-pandemic reality. If yours is as well and you want to do something, offer an accident plan to your employees or if you’re an employer, consider paying for it as a plan that’s less than a dollar a day can deliver so much…it’s unbelievable.

The Accident Plan…so easy to love.

Pamela